Lecture

讲座会议

Report

报告著作

-

数字金融:数字化的金融强国之路《数字金融:数字化的金融强国之路》由黄益平、黄卓、谢绚丽主编。本书对如何做好数字金融这篇大文章、走好数字化的金融强国之路进行了分析和探讨,指出我国的金融强国建设就是一条数字化的金融强国之路。2025.11.04

数字金融:数字化的金融强国之路《数字金融:数字化的金融强国之路》由黄益平、黄卓、谢绚丽主编。本书对如何做好数字金融这篇大文章、走好数字化的金融强国之路进行了分析和探讨,指出我国的金融强国建设就是一条数字化的金融强国之路。2025.11.04 -

数字金融(新文科数字经济系列教材)数字金融(新文科数字经济系列教材)由黄益平、黄卓、沈艳 主编。本书全面梳理了数字金融的全球发展概况、业务模式、基础设施及其对经济和市场的影响。全书分为16章,具体内容包括:第1章为导论,介绍数字金融基本概念和本书特色。第2章讨论数字金融的国际发展格局,涵盖其总体趋势、区域发展及关键影响因素,并分析各地案例。第3-11章聚焦不同业务模式,包括数字支付、征信、信贷、供应链金融、财富管理、保险和数字货币等,探讨其发展历程、创新技术及监管挑战;其中特别关注中国经验,如中国的数字支付、个人征信和大科技信贷案例。第12-14章着重论述数字金融中的大数据分析与治理、监管政策及测度方法。第15-16章探讨数字金融对金融市场和经济发展的影响,从交易成本到宏观政策传导,再到收入差距和数字鸿沟,全面分析数字金融的潜力与挑战。 本书以翔实的案例和数据分析构建了数字金融的研究框架,可作为高等院校经济金融类专业本科生教材,也可作为从业者深入了解数字金融前沿问题的参考书。2025.08.22

数字金融(新文科数字经济系列教材)数字金融(新文科数字经济系列教材)由黄益平、黄卓、沈艳 主编。本书全面梳理了数字金融的全球发展概况、业务模式、基础设施及其对经济和市场的影响。全书分为16章,具体内容包括:第1章为导论,介绍数字金融基本概念和本书特色。第2章讨论数字金融的国际发展格局,涵盖其总体趋势、区域发展及关键影响因素,并分析各地案例。第3-11章聚焦不同业务模式,包括数字支付、征信、信贷、供应链金融、财富管理、保险和数字货币等,探讨其发展历程、创新技术及监管挑战;其中特别关注中国经验,如中国的数字支付、个人征信和大科技信贷案例。第12-14章着重论述数字金融中的大数据分析与治理、监管政策及测度方法。第15-16章探讨数字金融对金融市场和经济发展的影响,从交易成本到宏观政策传导,再到收入差距和数字鸿沟,全面分析数字金融的潜力与挑战。 本书以翔实的案例和数据分析构建了数字金融的研究框架,可作为高等院校经济金融类专业本科生教材,也可作为从业者深入了解数字金融前沿问题的参考书。2025.08.22 -

数字金融前沿文献导读《数字金融前沿文献导读》由北京大学谢绚丽教授主编,北京大学出版社于2024年5月出版。该书聚焦数字技术对金融行业的革新作用,系统梳理国际学界在数字金融领域的最新研究成果。2024.05.31

数字金融前沿文献导读《数字金融前沿文献导读》由北京大学谢绚丽教授主编,北京大学出版社于2024年5月出版。该书聚焦数字技术对金融行业的革新作用,系统梳理国际学界在数字金融领域的最新研究成果。2024.05.31

Research

学术研究

-

数字金融助推“一带一路”国家小微企业成长本文以各国移动支付平台的推出为准自然实验,基于中国参与通信领域国际公共产品供给的视角,考察数字金融对“一带一路”国家小微企业成长的影响。研究发现,数字金融助推“一带一路”国家小微企业成长水平提升9.35%,且该效应随中国通信项目援助增加而增强。原因在于中国通信项目援助通过扩大国际公共产品供给,提高了“一带一路”受援国信息基础设施水平,进而通过“质量效应”与“成本效应”增强小微企业技术可及性,弥合数字金融发展中的数字鸿沟。此外,数字金融通过改善融资环境、优化社会信用环境和提升资金配置效率促进小微企业成长,这些机制在受援国更为显著。2025.11.30

-

Digital institutions and virtual involvement of born-digital firmsBorn-digital firms increasingly pursue virtual involvement, a digital market-entry strategy that prioritizes iterative data collection and algorithmic adaptation over physical expansion. We measure virtual involvement by the number of unique digital advertisements and define it as the intensity of a firm’s digital experimentation to collect user data, train algorithms, and enable continuous learning through a recursive feedback loop. Using a novel panel dataset covering 194 US and Chinese born-digital firms across 33 countries from 2016 to 2022, our empirical analysis finds that stringent host-country digital privacy regulation significantly reduces virtual involvement. This negative influence is weakened in larger digital markets, for firms from home countries with robust digital regulatory regimes, and when firms receive positive public sentiment. These results extend institutional theory and non-traditional entry mode research by introducing virtual involvement as a new dimension of international strategy under regulatory constraints. For policymakers and managers, our study offers actionable guidance: strict privacy rules protect user welfare, but supportive market conditions and regulatory experience are critical to sustaining data-driven innovation. Policymakers should balance user protection with market dynamism, while firms should leverage large markets and positive sentiment to maintain their virtual involvement.2025.11.18

-

Does FinTech reduce human biases? Evidence from advisory vs. automated FinTechs in lendingWe investigate whether FinTech can mitigate human biases in lending decisions using proprietary loan-level data from a Chinese auto equity lender. The lender first integrated big data credit scoring as an advisory tool to enhance its traditional lending model, subsequently transitioning to algorithmic decision-making with optional human override. Our findings reveal that cognitive biases decrease significantly when loan officers use algorithmic lending decisions, substantially reducing disparities in loan-to-value ratios between local and nonlocal borrowers without exacerbating default differentials. Notably, the discretionary adjustments made by loan officers remain modest. In contrast, advisory credit scores alone exhibit no discernible bias-reducing effects. Our study is among the first to demonstrate that automation and choice architecture – specifically, nudging via algorithmic defaults – is more effective than mere information provision in combating discrimination and promoting financial inclusion.2025.10.22

-

Market accessibility and poverty alleviation: Evidence from ChinaUsing village-level data from Guangdong Provincse’s targeted poverty alleviation campaign (covering 13,802 villages), this study exploits the rollout of the “E-commerce into Villages” program as a quasi-natural experiment and applies a staggered difference-in-differences strategy to assess how improved market accessibility affects the orientation and effectiveness of poverty alleviation. Results show that the program significantly enhances poverty reduction outcomes. Mechanism analysis reveals that enhanced market access shifts policy emphasis toward development-oriented approaches and away from subsistence-based support, thereby stimulating the aspirations and productive behavior of the rural poor. Heterogeneity analysis further indicates stronger effects in villages with more cadres from enterprises or developed cities, and in less-developed areas. Finally, evidence suggests that improving market accessibility—emphasizing capacity building over direct transfers—supports sustained rural development. These findings highlight the importance of e-commerce as a tool for promoting inclusive growth and effective poverty alleviation in developing countries.2025.10.01

Research

指数编制

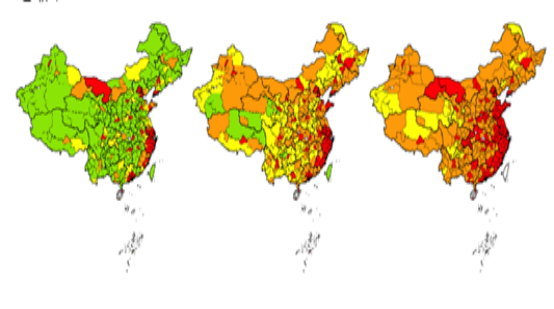

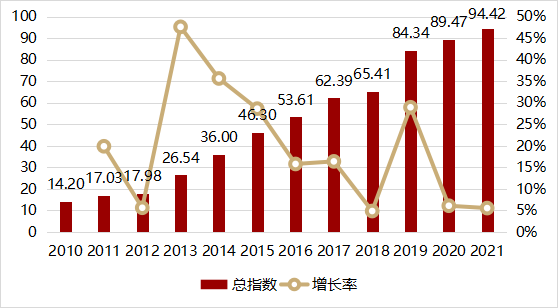

北京大学数字普惠金融指数

北京大学数字普惠金融指数,由中心研究团队与蚂蚁集团研究院合作编制,包含31个省、338个地级市以及约2800个县的2011-2021年数字普惠金融指数,并细分为数字金融覆盖广度、数字金融使用深度和普惠金融数字化程度等分指数。指数研究团队主要成员包括:郭峰、王靖一、程志云、李勇国、王芳等。

北京大学商业银行数字化转型指数

北京大学中国商业银行数字化转型指数,由中心研究团队独立完成,现已更新至第三期。该指数从战略数字化、业务数字化和管理数字化三个维度,对 2010-2021年至少具有三年完整数据的银行进行指数的构建。最终进入指数排名的银行共 246 家,包括全部 6 大国有银行,12 家股份制银行,以及 128 家城市商业银行、54家农村商业银行,29家外资银行,以及 17 家民营银行。